Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

This consolidated update gives a brief overview of developments in the last six months in UK public M&A.

We discuss:

1. Public M&A activity in the UK

Whilst there was an uptick in firm offers in Q4 of 2024, the start of 2025 was quieter. This could be down to the ongoing geopolitical uncertainty.

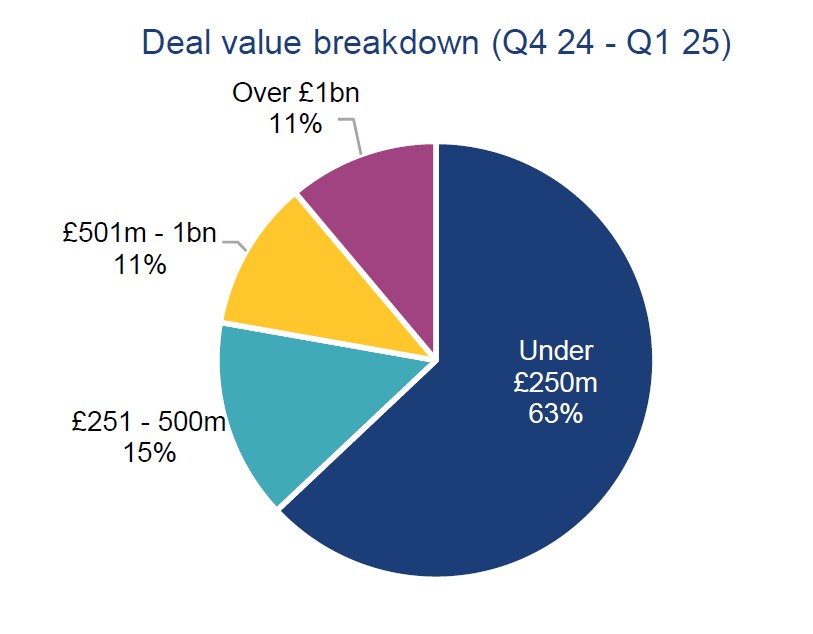

Activity was mainly confined to small-cap companies, with fewer large value deals in Q4 2024 and Q1 2025 compared to the previous six months – 17 of the 27 offers were for £250 million or less, while only three were worth over £1 billion (a significant drop from the 10 £1 billion+ deals seen in Q2 and Q3 of 2024).

2. The bidders

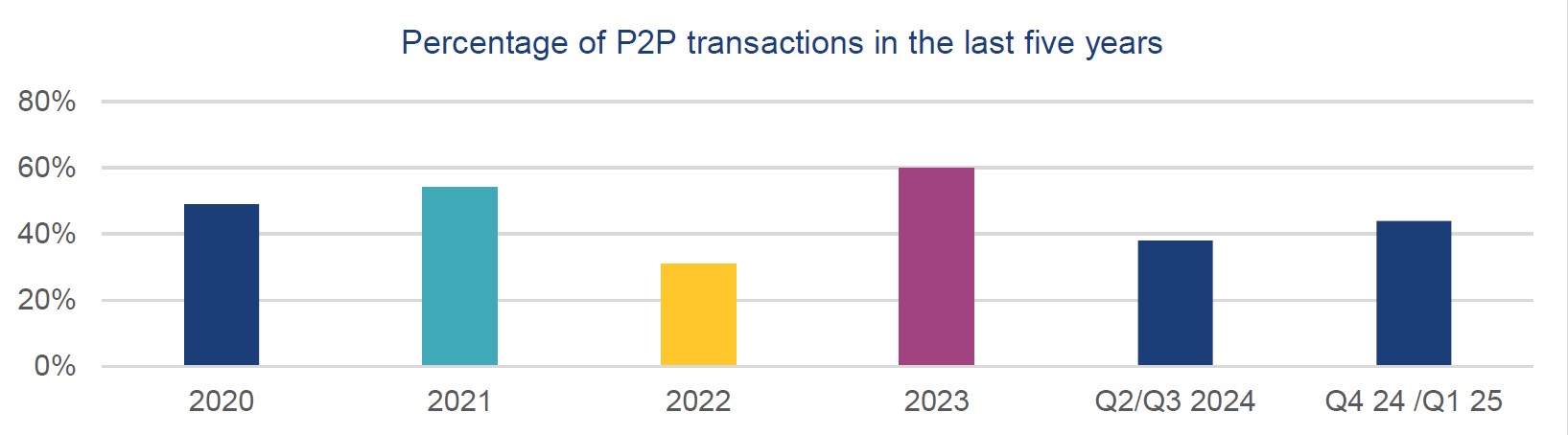

Strategics were behind 52% of firm offers announced in the six months ended 31 March 2025, compared to 62% in the previous six months.

The increase in firm offers that were public to private bids – rising from 38% in Q2 and Q3 2024, to 44% of offers in Q4 2024 and Q1 2025 – suggest that sponsor bidders are seeing more opportunities to purchase undervalued assets. Examples so far this year include the offer for Renewi plc by Macquarie Asset Management Europe and British Columbia Investment Management Corporation and HSQ Investment Limited's offer for Kingswood Holdings Limited.

3. Consideration

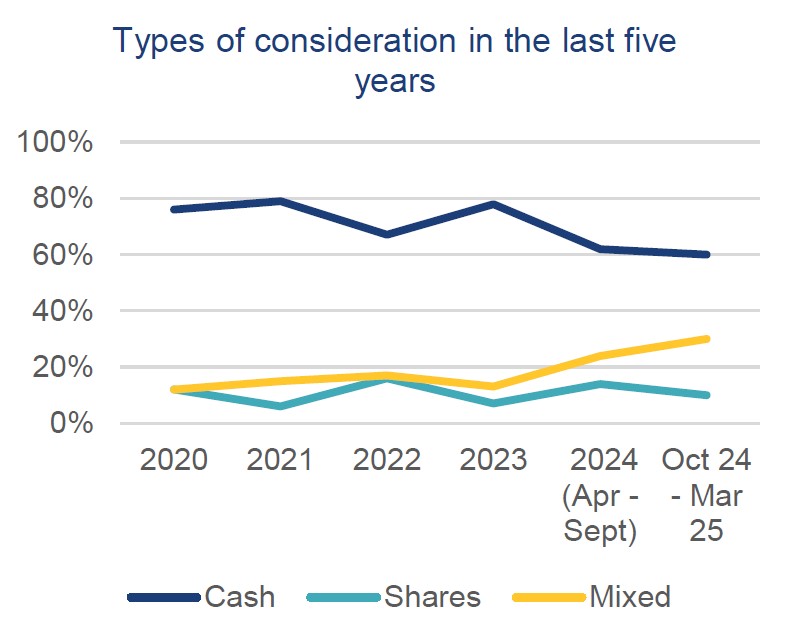

The proportion of bids offering all-share consideration in the six months to April 2025 reduced to 10%, down from 14% between April and September 2024. There has, however, been an increase in bids offering a mix of consideration, hitting a five year high at 30%, a 6% increase compared to the levels seen between April and September 2024.

As bidders adapt to the current geopolitical environment, alternative consideration options continue to be explored to bridge gaps in valuation expectations. There have been four offers with an unlisted securities alternative and another four where the consideration was cash and shares, with two having an all-share alternative.

1. Changes to the companies to which the Takeover Code applies

The Takeover Panel has narrowed the types of companies to which the Takeover Code applies, to focus on UK companies which are, or have in the last two years been, quoted in the UK (see RS 2024/1).

The changes, which were broadly in line with the Panel’s proposals in its consultation paper PCP 2024/1, took effect on 3 February 2025. The principal change to the amendments proposed in the consultation paper is that the length of both the run-off period and the transition period is two years, rather than the three years originally proposed.

Companies that are subject to the Takeover Code under the new rules

Under the new rules, the Code applies to a company if it has its registered office in the UK, the Channel Islands or the Isle of Man and either:

Companies that are no longer in scope

The Code no longer applies (subject to the transitional provisions discussed below) to:

Other points to note

We discussed the rule changes in this episode of our public M&A podcast series.

2. FCA Primary Market Bulletin 52 on takeover approaches and the Market Abuse Regulation

The Financial Conduct Authority (FCA) published a Primary Market Bulletin (PMB 52) on inside information. One of the topics it covers is whether the receipt of an approach about a possible takeover offer is inside information for the purposes of the UK Market Abuse Regulation (UK MAR).

The FCA says it has seen cases where companies have been advised that inside information crystallised only when a final offer was accepted by the company’s directors, because the likelihood of the transaction taking place before that point was not deemed certain.

It says that whether the receipt of an offer is inside information should be assessed on a case by case basis. Relevant factors to take into account could include the identity of the bidder, the nature and quantum of the offer and the likelihood that the offer will be recommended by the board of the listed or traded target company.

The clear reminder is that an approach can be inside information before it has been formally considered and recommended by the board.

We discuss PMB 52 in this episode of our public M&A podcast series.

3. FCA Primary Market Bulletin 54 on leaking inside information during M&A

The FCA published another Primary Market Bulletin (PMB 54) which focuses on strategic leaks during M&A transactions and the fact that a leak may involve the unlawful disclosure of inside information.

The FCA says that it has seen an increase in situations where material information on live M&A transactions appears to have been deliberately leaked to the press. Examples of the information leaked include details of discussions between the board of a target company and a potential bidder following an approach about a possible takeover offer, or where the target board has rejected an approach but an increased offer is likely.

It notes that the leak of inside information may be inadvertent, by hinting at market sensitive information even if specific details are not mentioned, or strategic, where the information is deliberately given to the press by individuals at an issuer or its advisers. The FCA is concerned that there is a culture among market participants that strategically leaking inside information to the media is acceptable during a transaction.

The FCA reminds parties that the information being leaked is often inside information under UK MAR and that UK MAR prohibits the unlawful disclosure of inside information. Unlawful disclosure is where a person possesses inside information and discloses that information to any other person, “except where the disclosure is made in the normal exercise of an employment, a profession or duties”.

The FCA warns individuals directly involved in transactions that:

It also reminds issuers and their advisers that:

We discuss PMB 54 in more detail in this episode of our public M&A podcast series.

4. Changes to the UK merger control regime

The thresholds at which the UK merger control regime is engaged changed as of 1 January 2025.

The Digital Markets, Competition and Consumers Act 2024 (Commencement No.1 and Savings and Transitional Provisions) Regulations 2024 brought into certain provisions of the Digital Markets, Competition and Consumers Act 2024 (DMCC Act) including the thresholds at which the UK merger control regime is engaged.

When the UK merger control regime will be relevant

The Competition and Markets Authority (CMA) has jurisdiction over “relevant merger situations” in the UK. Following the 1 January changes, a transaction will give rise to a relevant merger situation where two or more enterprises cease to be distinct and:

Under the other changes made by the DMCC Act:

These provisions apply to any transaction that had not completed (or where the CMA had not launched a formal investigation) before 1 January 2025.

Other changes to the UK merger control regime

Other changes to the regime that came into force on 1 January 2025 include:

Other areas covered by the DMCC Act

The scope and implications of the DMCC Act are wide-ranging. In addition to merger control, other key reforms introduced by the DMCC Act include implementing the UK’s new digital markets regime, which will see technology firms with strategic market status having their conduct regulated by the CMA and subject to a new mandatory merger reporting requirement, and strengthening the CMA’s role in the enforcement of consumer protection legislation.

For more information on the DMCC Act, see our Competition, Regulation and Trade ebulletin.

5. Takeover Panel obtains court order to secure compliance with ruling to pay compensation

The Takeover Panel has obtained a court order to secure compliance with the Hearings Committee ruling (see Panel Statement 2024/16 published in July 2024) that three former members of management in MWB Group Holdings pay compensation to the former shareholders of the company (Panel on Takeovers and Mergers v Mr. Richard Gary Balfour-Lynn & ors [2024] EWHC 3044 (Ch)).

The individuals were found to have breached Rule 9 of the Takeover Code. Whilst the Panel Executive would ordinarily have required a Rule 9 offer to be made by the concert party members to the other MWB shareholders, the Executive took the view that, as MWB had been liquidated in 2013 and removed from the Register of Companies in 2018, it was impracticable, if not impossible, to restore MWB to the Register with a view to reconstituting the company and requiring the Rule 9 offer. It therefore sought a compensation order as an alternative. For more information, see the post here.

Under section 955 of the Companies Act 2006, the Panel can apply to court to secure compliance with its rulings. This is only the second time the court has been asked to make such an order under section 955. The first order was sought by the Takeover Panel to secure compliance with a ruling that David King make a mandatory offer for Rangers plc. In granting the order in that case, the court said that if the Panel issues a ruling, the court will enforce it in the absence of exceptional circumstances, and any decision not to enforce a Panel ruling would be rare, with the “most obvious case where enforcement might be refused is where material changes in circumstances have occurred subsequently to the last decision” by the Panel.

In this case, the judge (Chief Insolvency and Companies Court Judge Briggs) said that the discretion provided to the court is large. Although the factual matrix may persuade a court to make any section 955 order in the majority of cases, there will be circumstances where the discretion will be exercised against making such an order. He went on to say that he did not think it helpful to add additional language to the statutory wording such as 'in exceptional circumstances', 'very exceptional circumstances' or 'rare cases'. The court will have to balance relevant factors in the usual way. He gave some factors that may carry weight, both in favour of and against an order.

We discuss the court order in this episode and the original ruling in this episode of our public M&A podcast series.

1. Our top tips for navigating public M&A in the UK

Public M&A in the UK operates in a highly regulated and uniquely challenging environment. Success often depends on understanding the nuances of the UK Takeover Code, anticipating shareholder dynamics, and crafting strategies that align with both regulatory requirements and commercial objectives.

We have launched a video series, in which members of our UK public M&A team offer insights to help bidders, investors, companies and shareholders navigate the complexities of UK public transactions.

In the videos, we give top tips for:

Click here to watch the videos.

2. Our UK public M&A podcast series

All episodes in our public M&A podcast series, in which we consider key trends, developments and topical issues seen on public M&A transactions in the UK, are available on our public M&A podcast page.

Topics covered in recent episodes – in addition to those mentioned above – include:

3. Our 2025 global M&A report

In January, we published our annual global M&A report titled ‘Global M&A Outlook for 2025: Gaining Altitude'.

Looking back at 2024, we asked if the M&A market was ready for take-off. The answer? Not quite. Challenges like inflation, geopolitical tensions, and rising costs persisted, with recovery driven largely by big-ticket deals rather than widespread activity.

Our report reflects on the efforts required to launch deals in 2024, and the anticipation (written before the US position on tariffs became clear) of a surge of activity in 2025.

In particular, we look at:

We also shared regional perspectives from our teams around the world, in which we looked at regional trends in M&A and the outlook for 2025 and our sector and broader perspectives in which we look at sectoral and wider trends in M&A.

4. M&A – UK Guide

We have authored the UK chapter of the International Corporate/M&A Practice Area Guide published by Global Law Experts.

We discuss matters such as:

You can read the chapter here.

5. Our Takeovers Portal

All of the resources mentioned in this update, and more, are available on our Takeovers Portal.

What is it?

The Portal contains various materials which will assist you in understanding and advising on takeovers, including our latest thinking on public M&A, specific and general guides to takeovers as well as some useful precedents, all accessible in one place.

What is on the Portal?

The Portal is divided into four sections:

The Portal also provides links to the Takeover Code, Panel Practice Statements and Panel checklists and has a facility to ask questions.

How do I access it and subscribe for updates?

You will need to register to receive access to the Portal. Once your registration has been approved, you will be free to access it and can subscribe to receive notifications of any updates to the latest thinking on the Portal.

Please click here to begin your registration.

Accessing the Portal from your phone

To put a shortcut to the Portal on the home screen of your mobile device, open the Portal (https://hsfnotes.com/takeovers) and:

Partner, London

Partner, London

Partner, Head of M&A, London

Partner, London

Knowledge Counsel, London

Partner, London

Partner, London

Partner, London

Partner, London

Consultant, London

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead