Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

We have run our annual analysis of announced non-binding indicative offers and pre-bid stakes in public M&A to capture NBIOs announced in calendar year 2025.

Our NBIO analysis is timely after the Takeovers Panel this month looked closely at the disclosures made in respect of an NBIO received by Humm Group relative to the target’s communications to the bidder. In that matter, the Panel considered that the public disclosure by the target had misled the market about the true state of the engagement between the parties. That could become a factor when Boards are deciding when to disclose receipt of an NBIO: if it is disclosed later in the piece, more details may need to be disclosed about the level of engagement after the NBIO was received.

Our review of NBIOs and pre-bid stakes announced in 2025 reveals the following:

We have analysed the NBIOs announced by public companies during calendar year 2025 against the previous 4 year averages. The conclusions from the data provide valuable insights on evolving trends for both targets and bidders when formulating strategies.

This analysis builds on the following articles we published during 2025:

The previous articles above discuss the law and reasoning for some of the strategies adopted. We have not restated the law and strategy in this article – instead focussing on the changes in strategies and outcomes and their possible drivers.

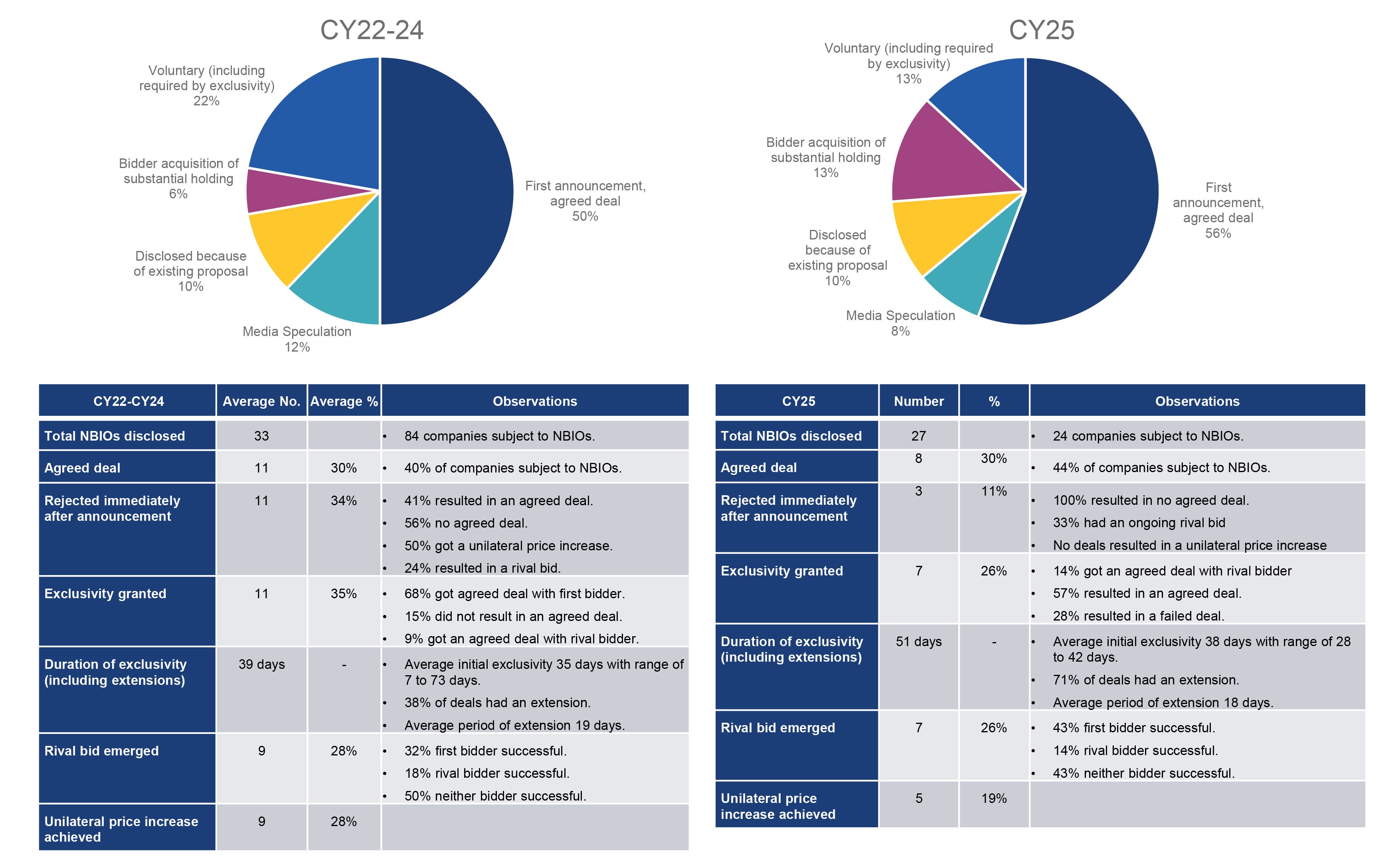

NBIOs disclosed before binding agreements were slightly down on previous years, with 27 in CY25 relative to an average of 33 for CY22-24.

The overall success rates were steady in CY25, at 30% of NBIOs or 44% of targets approached (CY22-24 average was 30% and 40%, respectively).

The reasons for disclosure of an NBIO were broadly consistent in CY25 with previous years.

Once again, the majority of NBIOs were not announced before a binding implementation agreement, reinforcing the preference for bidders and targets to deal confidentially and only reveal an approach if and when a deal is agreed.

Media leaks continued to represent a small percentage of the reason for disclosing an NBIO, 8% relative to last year’s 12%. Voluntary disclosure was again the main reason for early disclosure of NBIOs, driving disclosure in 13% of instances, against 22% for the average in CY22-24.

The risk of a rival bid was consistent, occurring in 26% of cases in CY25 (against an average of 28% in CY22-24). Again, in the majority of cases where there were multiple bidders, no bidder was successful – a bitter pill to swallow for target shareholders watching on as the NBIOs played out publicly.

A bidder that moved first in a multiple bid scenario was most likely to be successful (43% of cases in CY25), supporting the conclusion that first movers have an advantage, or arguably have more conviction to win the day.

Anecdotally, due diligence and negotiation periods are extending.

Notable examples of extended due diligence and negotiation phases last year include:

The duration of exclusivity periods are a proxy for the time taken to conduct due diligence and negotiate transaction documents. In CY25 exclusivity periods were longer.

The average duration of exclusivity (including any extensions) increased to 51 days in CY25 relative to the average of 39 days in CY22-24 (i.e. a 30% increase). While the average initial exclusivity periods and periods of extension in CY25 were broadly consistent with prior years (38 and 18 days versus CY22-24 averages of 31 and 19 days, respectively), extensions were granted in more cases in CY25, occurring in 71% of deals compared to 36% of the time on average over CY22-24.

These longer engagement periods are to be expected in uncertain times. Bidders are proceeding with more caution, taking more time to work their way through due diligence, while retaining optionality over their deals. They are being more thorough in due diligence and allowing more time to absorb the volatility in news flow that, for now, seems to be an important and constant part of the deal landscape to navigate.

Extended due diligence and negotiation periods while an NBIO is public presents a significant challenge for targets. Their share price typically trades on an assumption that the deal is done, when this may be an overconfident position from the market (as the Santos example highlights). Further, this period of limbo in ownership can be disruptive to the business of the target, with the uncertainty unsettling employee and customer bases, while distracting management from running the business.

What can targets do in the face of these extended engagement periods and the disruption risk? The best advice is to try to deal with an NBIO confidentially. If the NBIO is revealed, hold the bidder to account, setting clear deadlines for outcomes. Also, pre-planning to be ready to facilitate due diligence in a timely manner by organising materials and being thoughtful about packaging and releasing information. Make no mistake, controlling the timetable is an important tool for success.

In only 11% of instances in CY25 the target rejected an NBIO immediately after its announcement. This is significantly lower than the 34% in CY22-24. Have target Boards become more willing to entertain a bid?

Part of the explanation for this is that there was a near doubling of the percentage of NBIOs announced because the bidder had acquired a substantial holding alongside making its bid and was required to disclose its position. We have seen a notable uplift in bidders seeking to protect their deal at the time of first approach, through acquiring a substantial holding (more on this later).

It is much harder for a target to outright reject an NBIO where the bidder either has shareholder support or a foot on a pre-bid stake. That is an important lesson for bidders from the empirical data.

The decline in immediate rejections may also be driven by greater macroeconomic uncertainty. Fundamental value and what is in the best interests of shareholders may be a closer call when the future is not as certain. This will continue to be a factor in the current geopolitical climate.

The Takeovers Panel’s decision this month in the Humm Group matter is a timely reminder on avoiding misleading disclosures in this context. The Panel found that the target had misled the market by communicating to the bidder that the offer price did not meet value expectations, while communicating to the market that it was engaging on the NBIO. There’s a fine line for target boards wanting to be seen to engage with a bidder, while negotiating for a better price.

This year, we have expanded the analysis to answer the question: when is a target more likely to get an NBIO?

Of the CY25 NBIOs:

The data supports the conventional wisdom, that management instability, earnings downgrades and significant corporate developments are key drivers for a takeover approach. Companies staring into such announcements should be prepared, as the risk of an NBIO being received is heightened in these periods.

1For one transaction (CC Capital Partners LLC / Insignia Financial Ltd) price chip occurred despite offer price exceeding initial offer price (reflected as price bump).

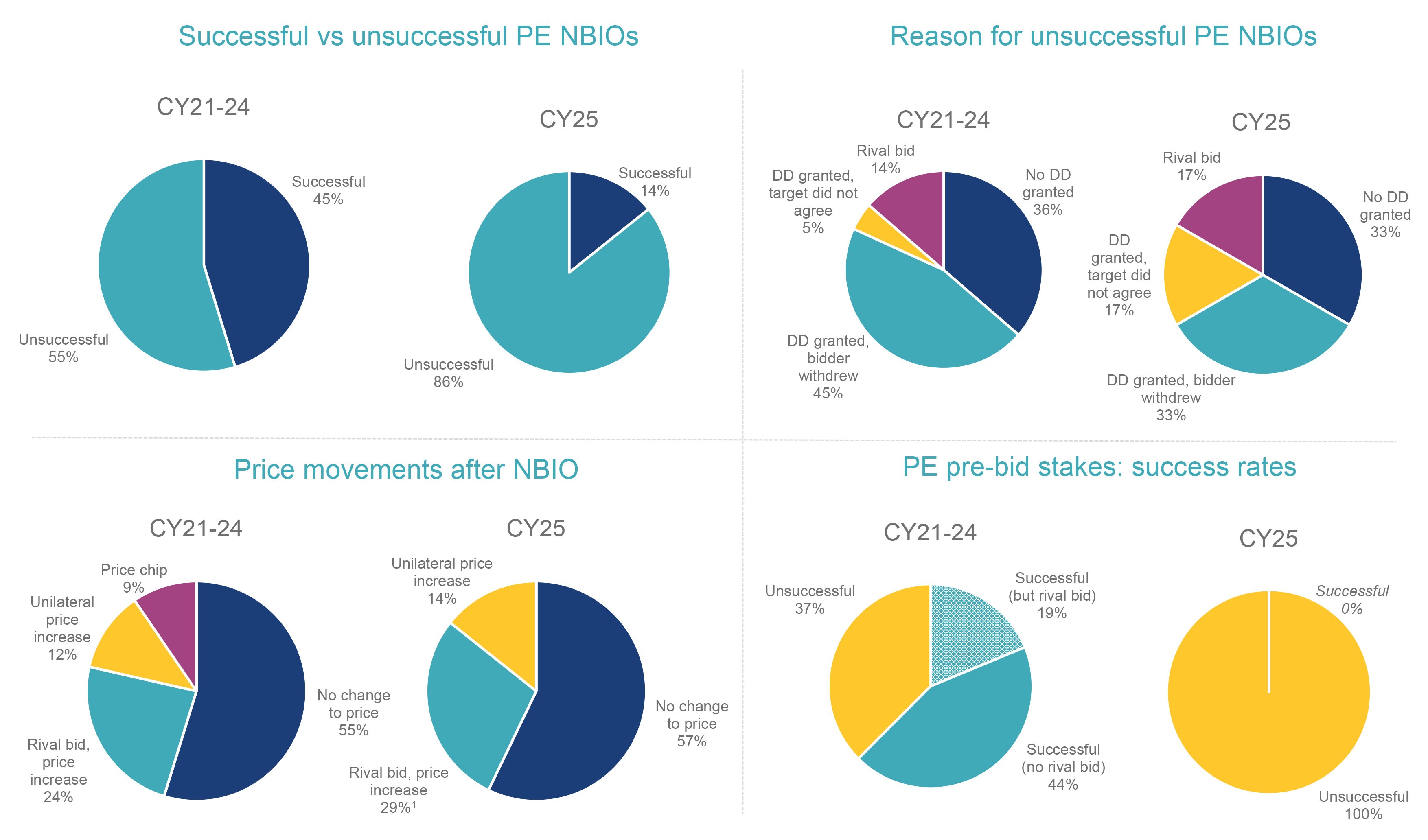

Private equity NBIO success rates see-saw materially from time-to-time. The CY22-24 period saw particularly high success rates.

Conversely, CY25 saw a significant decline in PE success rates, with only 14% of announced NBIOs resulting in an agreed deal (versus an average success rate of 45% in CY22-24 for this bidder set).

It is not a lack of competition for targets, with 17% of situations drawing another bidder (versus an average of 14% for CY22-24).

33% of the PE bidders in CY25 were not granted access to due diligence, which is in line with the average of 36% across CY22-24.

Either target Boards felt emboldened to hold the line on value expectations or PE bidders were more disciplined in their offer prices.

14% of PE NBIOs resulted in a unilateral price increase (versus an average of 12% for CY22-24). So, it seems that PE bidders were not less willing to bid up for an asset.

One explanation is that PE bidders in CY25 timed their run to coincide with low points in share trading following unfavourable target news, while target Boards looked through the near term trading softness to reject the offer. Examples of this include:

Again, in CY25, a large percentage of PE bids did not proceed when the bidder withdrew during due diligence (33%). The notable example was EQT and CVC’s bid for AUB.

There is always room for debate as to what causes these to fall-over. From time to time target Boards can push PE bidders to the limit on price with reference to publicly available information. The pre-due diligence negotiation can leave little margin for error on valuation based solely on publicly available information. We get that Board’s lose significant bargaining power once they allow access to due diligence, front loading price negotiations.

Although not in our data set - Challenger’s and KKR’s bid to take Pepper Money private saw a significant offer price reduction during due diligence. The change in interest rate expectations presumably saw the bidders reassess fair value during due diligence.

The other interesting development was that all PE NBIOs where the bidder had pre-bid stake were unsuccessful (including both the examples above). For CY25 at least, it seems the pre-bid stake was not effective for PE bidders in forcing the hand of the target to engage. Notably, in all of those cases the PE bidder still retains their stake – so it may be too early to call it over in all of those cases.

1. Analysis restricted to control transactions involving an ASX-listed target where implied equity value >$250m, live deals have not been included in these statistics.

2. For CY22-24, of the bids with direct holding, 12% of them were also combined with a voting intention statement.

3. For CY22-24, of the bids with a call option, 40% of them were combined with a voting agreement. A further 40% were combined with a voting intention statement.

4. For CY25, of the bids with direct holding, 17% of them were combined with a voting intention statement. A further 8% were combined with a voting agreement.

5. For CY25, of the bids with a call option, 33% of them were combined with a voting intention statement.

CY25 continued the trend of bidders with pre-bid stakes being more likely than not to get to an agreed deal.

On 15% of occasions a bidder with a pre-bid stake was foiled by a rival bid, which is broadly in-line with the average for CY22-24 (12%).

Interestingly, of the successful bidders with pre-bid stakes in CY25, 91% did not need to increase their price. This was much higher than the average for CY22-24 (45% of cases). Arguably, this indicates that bidders with pre-bids were more resolute in not being negotiated up on price.

However, there was a significant increase in bidders with pre-bid stakes being unsuccessful absent a rival bid – this was 30% of cases in CY25, versus the average of 5% in CY22-24. We conclude that pre-bid stakes were less effective in CY25 in driving success. What drove that?

Note: bids that were unsuccessful are highlighted by the patterned shading.

Drilling into the form of pre-bids, we see direct holdings (i.e. shares actually purchased) as still the dominant form, representing 65% of pre-bids against the prior 4 year average of 58%. Interestingly, more than half of the instances in CY25 where there was a direct holding resulted in an unsuccessful deal (well up from an average of less than 10% in CY22-24).

Notable examples of direct holding pre-bid stakes not succeeding include:

In each of these instances, except one, the bidder continues to hold the pre-bid. Perhaps it is too early to close the book on some of these situations. With the passage of time, the bidder may eventually become successful, improving the conversion rate.

Call options were used in 15% of pre-bids in CY25 (in line with the prior 4 year average of 12%). Once again, every instance of a bidder using a call option resulted in a successful deal. A 100% success rate. This reinforces the effectiveness of call options as a pre-bid stake (if you can get them).

The statistics in the review of NBIO and pre-bid stakes in 2025 provide useful insights for both bidders and targets. The climate shifted in CY25, and our comparison to average outcomes in CY22-24 arms bidders and targets on the emerging trends.

If you have any queries regarding the data or specific situations, please do not hesitate to contact us.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead