Stay in the know

We’ll send you the latest insights and briefings tailored to your needs

Subscribe now

Cyber security is a major compliance issue for global payment services.

The technology advances in payment services and the use of online and mobile payments, electronic storage and global communications systems creates increased efficiencies in payment services, but with an increased risk from cyber security breaches. The recent 2014 Cost of Data Breach Study by the Ponemon Institute covering Australia and other countries highlighted that Australian companies in the financial services sector along with the retail sector are more likely to suffer a breach in contrast to other sectors of the economy.

Whilst companies can implement measures to prevent cyber-attacks from being successful, they cannot guarantee that those measures will be successful. Cyber security policies must cover not only prevention but post-breach mitigation.

Significant business impacts can flow from cyber security incidents. The most obvious are:

The financial impact of cyber security breaches is highlighted in the 2014 Cost of Data Breach Study by the Ponemon Institute. Taking Australia as an example, it notes the average cost of a data breach paid by a company in 2014 was AUD 2.8 million. Additionally, average churn rates have increased by 5% meaning more customers were terminating their customer relationship following a data breach.

Security breaches affecting payment services are likely to be more costly, than other breaches in particular as result of the cost of managing fraud. Perhaps the most widely known cyber security breach affecting payment services was in 2014 when 40 million credit card numbers and the personal information of 70 million individuals were reported to have been stolen from the US retail chain Target through the installation of malware in Target’s security and payment system.

In our experience, where a cyber security incident arises, several steps should be taken by the affected organisation to mitigate the impact on individuals, the organisation itself and other stakeholders.

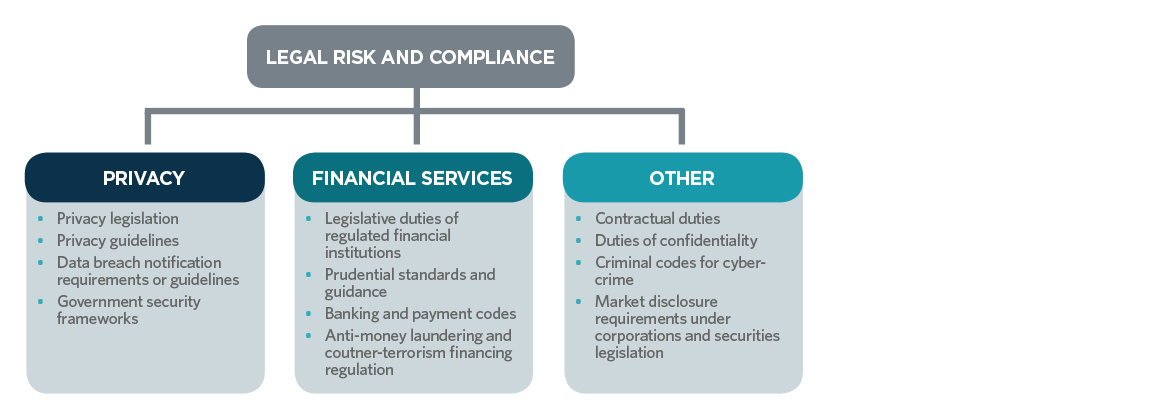

There is no single piece of legislation or regulation that addresses cyber security holistically. In the payment services sector, relevant legislation covers a wide range from privacy legislation, financial services legislation, corporations and securities legislation to common law duties of confidentiality and cyber-crime offences under criminal codes.

The legislative framework is also heavily supplemented by guidance on recommended practice produced by privacy and financial services regulators. A key part of the legislative and regulatory framework relates not only to prevention, but also steps to be taken in the case of a breach.

In particular, data breach notification is a major legal and risk consideration, concerning duties or recommended practice to notify affected individuals, regulators, the market or crime enforcement agencies. The diagram below summaries the legislative landscape for cyber security.

Organisations providing or receiving payment services clearly need to have systems and procedures to manage cyber security risk and the impact on their business, customers, and individuals. Key steps in any cyber security risk mitigation strategy include:

Cyber security is likely to remain a major risk management factor in the global payment services industry. Its relevance was highlighted in the last month, with the publication of the Cyber Resilience Health Check, Report 429, March 2015 by the Australian Securities and Investments Commission (ASIC). This report is aimed at assisting ASIC’s regulated population improve their cyber resilience and is aimed at identifying how cyber security risks should be addressed as part of current legal and compliance obligations relevant to ASIC’s jurisdiction. The report’s publication is likely to increase the visibility of cyber security management at board level.

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

We’ll send you the latest insights and briefings tailored to your needs