Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

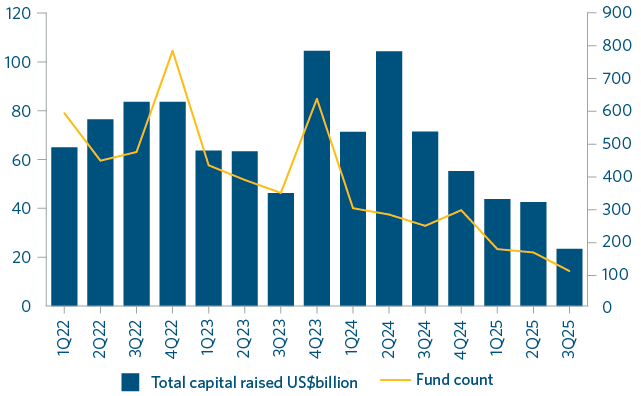

Asia private capital fundraising in Q3 recorded the lowest quarterly result in over 10 years.

Asia private capital fundraising continues to slow

Source: Pitchbook, based on closed funds.

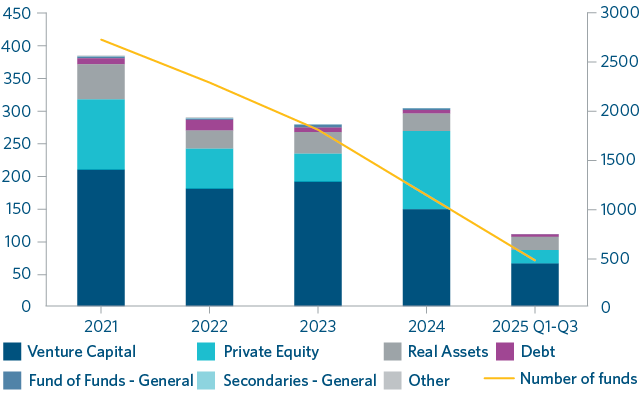

Steep contractions in private equity and venture capital fundraising caused the decline, down 82% and 60% respectively on the previous quarters.

Asia private equity fundraising has seen greatest decline after a strong 2024 (US$ billion)

Source: Pitchbook, based on closed funds.

There have long been concerns around a lack of distributions from private funds in Asia amid slow exit activity. The stubbornly subdued M&A and buy-out activity levels we mention below are the main reason for this. As discussed in our previous updates, market perception is that the lack of liquidity in the private M&A market hinders fundraising as LPs wait for distributions before re-deploying.

However, to put the figures for Asia into context, global macro trends are amplifying the downward trend. Asia's Q3 result reflects global fundraising totals, which are tracking at the lowest level in eight years.

"The Q3 data is a stark reminder that liquidity issues continue to plague Asia's private capital market," said Benjamin Lohr. "Unless we see a sustained upwards trend in M&A and buy-out activity in the market, we do not expect the fundraising environment to materially improve."

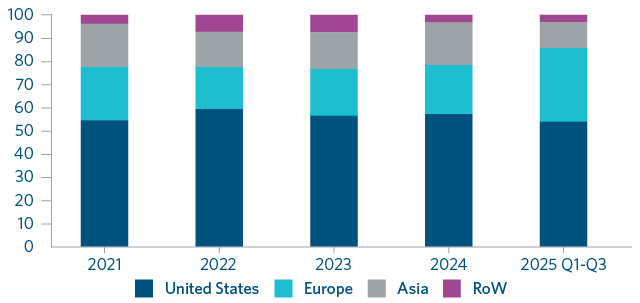

The long-expected moderation of US fundraising showed up in the data this quarter with the US's share of global fundraising for Q1-Q3 2025 now marginally below 2024.

While Asia's share of global fundraising is on track to contract markedly compared to 2024, Europe recorded the highest level of regional fundraising since 2007. Europe is emerging as a clear early benefactor of the moderation of allocations to the US, but probably also from the sluggish Asia fundraising market coupled with increased European interest from Asia investors.

Europe outpaces Asia and US in fundraising

Source: Pitchbook, based on capital raised by closed funds.

Asia private equity secondaries grew in Q3 to the highest level in five years, despite the tough fundraising environment, although fundraising for venture capital secondaries dropped back to 2022 levels.

While the Asia secondaries market is still disproportionately small compared to the US and European markets, it appears to continue to grow as an exit route for GPs with long holding periods for their private equity assets.

Continuation fund market has experienced significant growth

Global GP-led total transactions value ($bn)

Source: Schroders Capital, Guide to Continuation Funds: A market that has come of age.

GP-led transactions as a whole have grown significantly in size over the last few years. As reported by Schroders Capital, "interest has accelerated in today's muted exit environment." As shown in the table above, the segment has experienced compounded growth at roughly 27% per annum since 2013.

Additionally, and of very much interest at a time when investors are looking at increasing the pace of returns, Schroders reported that the average time to liquidity is about 18 months shorter for continuation funds than conventional buyouts.

"We remain of the view that secondaries, in particular GP-led secondaries and direct secondaries, can play a larger role in providing liquidity in the private capital markets in Asia," said Benjamin.

"While GPs are perhaps holding on to assets for now to wait for better valuations, specialist secondaries funds can play an important role in providing the necessary liquidity when they ultimately need to sell."

"From the investors' perspective, continuation vehicles offer attractive returns and a promise of liquidity."

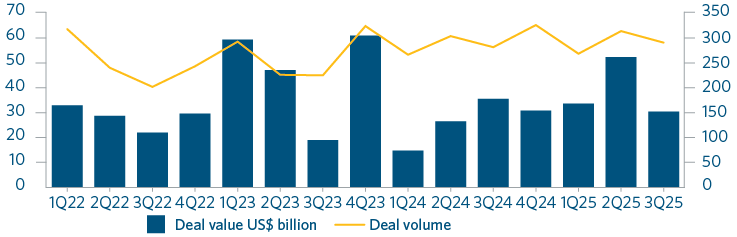

Q3 Asia buyout activity falls back after strong Q2

Source: Preqin

Encouraging signs from China, supported by the buoyant Hong Kong IPO market, are also evident in the Asian buyout market. China led the way in Q3 with its best performance in a number of years.

The expectation is for continued growth in both the VC and buyout markets in China with new technologies and healthcare active.

China leads Asia buyout activity in Q3

Source: Preqin, based on deal volume, US$ billion

In our Q1 analysis, we made a couple of predictions. Pricing expectations between buyers and sellers were closing, and EV/EBITDA multiples for Asia buyouts were tracking closer to major Asia indices, each of which might lead to increased exit activity.

Whilst we saw an uptick in Asia buyout activity in Q2, this has certainly dropped back again in Q3. Undoubtedly, macroeconomic and geopolitical uncertainty will have played its part (together with perhaps the summer holidays), but the predictions remain the same, especially in the small and mid-sized buyouts that are prevalent in the Asia market.

Small-mid buyouts trade well below large-cap and public peers

Consistent pricing in small-mid buyouts offers compelling entry points

Average entry EV/EBITDA multiples

Source: Schroders Capital, Private Equity Outlook Q3 2025: Three key levers to navigate uncertainty.

The relative entry point for small and mid-sized buyouts could create further exit and investment opportunities in Q4 in Asia. We are certainly seeing evidence of an uptick in the commencement of exit processes (both M&A and IPO led) and do see the market mood shifting.

However, execution risk remains and deals will continue to see longer lead times and greater internal scrutiny.

Disputes enquiries are rising markedly across the pipeline. "We're seeing another increase in pre-closing disputes, particularly where parties couldn't secure financing or wanted to adjust the price", said Kathryn Sanger.

"Advice on tightening terms to anticipate these types of issues is now crucial in any deal process."

Disputes are also likely from the emerging wave of potential exits on the redemption side. "It's not yet clear where the tipping point lies to activate these disputes, as parties weigh the costs of a dispute against potential returns," said Kathryn.

Lessons have been learned about the ease of exit, which in turn is increasing caution in structuring. Those investing at a later stage should build in access to legally accessible funds or other forms of investment return – a harder ask for early-stage VC investments with lower cash levels in the portfolio business.

|

Our Asia private capital team advises funds, asset managers, pension and sovereign wealth funds, and other institutional investor clients across the lifecycle. With expertise in seven offices across Asia, we advise on fund structuring and fundraising, through M&A, financing, consortium arrangements, asset management, and exits and disputes. Our sector focus adds value for clients with Asia market expertise in tech, financial services, consumer, infrastructure, energy/renewables, industrials and healthcare. Contact any of the partners below for access to the team's expertise, and click below to enrol for future briefings. |

Partner, Head of Disputes, China and Japan and Head of Private Capital, Asia, Hong Kong

Partner, Hong Kong

Senior Registered Foreign Lawyer (England and Wales), Hong Kong

Partner, Head of Private Capital, Asia, Singapore and Hong Kong

Partner, Head of M&A, Asia, Singapore

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead