Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

With the everchanging ESG regulatory landscape for funds, a lot of attention has been paid over the last years on how to build in disclosures, standards and protections required from ESG regulation into the fund documentation. At the same time, the documentation relating to a fund's investments has not received that level of attention. Often regulatory and strategy-related requirements are only covered by generic catch-all clauses to deliver "all required information" or take "all necessary actions" which are of limited use for investors and investees when push comes to shove. This is all the more difficult for impact investing strategies the ability for the investor and investee to work in an equitable manner to drive both financial returns and measurable environmental and/or social returns. Legal documentation can be an incredibly useful tool to ensure alignment between the investor and investee objectives and the contribution of the investee to the investor's dedicated impact goals.

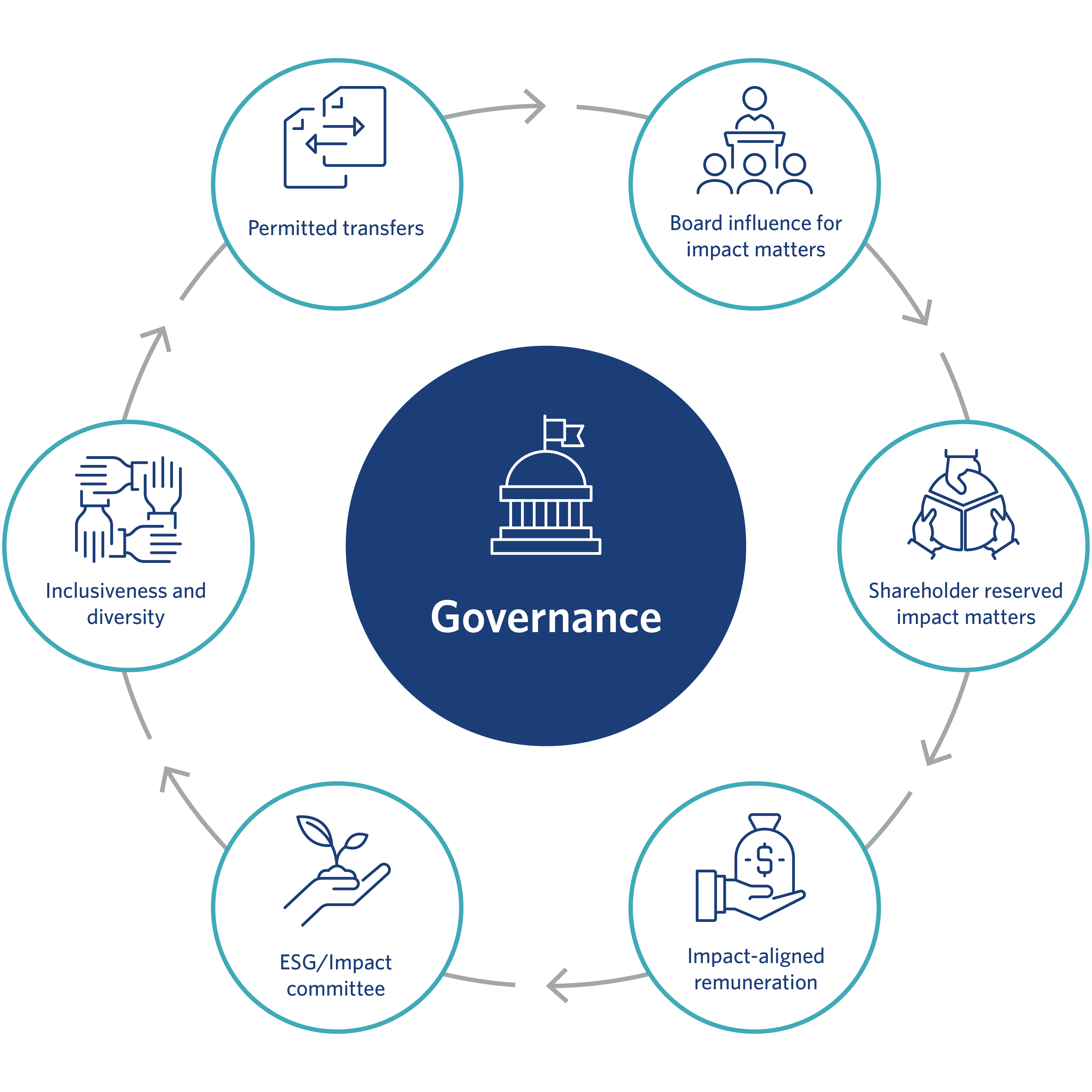

Impact specific provisions can be included in the investment documentation and traditional provisions can be adapted to really drive alignment. We have set out a few examples of provisions that can be altered to be considered "impact forward".

Most commonly:

These are just a few examples of deal terms that can be adapted for impact. As a firm, we are seeing more and more investors and investees that consider the benefit of such provisions to drive alignment and understand that defining the rules of the game upfront relying on legal creativity can be mutually beneficial and actively support the achievement of impact goals.

Partner, Germany

Partner, London

Partner, Luxembourg and Paris

Of Counsel, Madrid

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead