Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

In June 2026, there were nine Rule 2.7 announcements made across the UK public M&A market and three further possible offers announced.

Amendments to the EU Market Abuse Regulation (EU MAR), made by the EU Listing Act (2024/2809), took effect on 5 June 2026. The amendments relate to when inside information has to be disclosed where there are intermediate steps in a protracted process.

Both EU MAR and the UK Market Abuse Regulation (UK MAR) require issuers to disclose inside information as soon as possible (Article 17(1)). The key changes being made to EU MAR are as follows:

The changes mean that EU MAR and UK MAR are no longer aligned, and so issuers with securities listed in both the UK and the EU will need to consider their disclosure obligations under each of the Regulations separately. In particular they will need to remember that, in the UK, an intermediate step in a process that is inside information must be announced as soon as possible (unless the criteria for delaying disclosure are met).

ESMA is in the process of updating its guidelines on EU MAR, with publication expected in Q4 2026. The Financial Conduct Authority expects issuers to continue to apply the ESMA guidance in place at the time of the UK's departure from the EU to the extent that it remains relevant.

The EU Listing Act also makes changes to the EU Prospectus Regulation to allow, amongst other things, Member States to raise or lower the threshold for the requirement to publish a prospectus for public offers of securities between €5 million and €12 million.

June has marked the busiest month for deal activity so far in 2026, with nine firm offers announced. The number of possible offers is down slightly compared to the same period in 2025, down from five to three. The financial sector was particularly active during the month, accounting for three firm offers and one possible offer, underscoring its continued prominence in the current deal landscape.

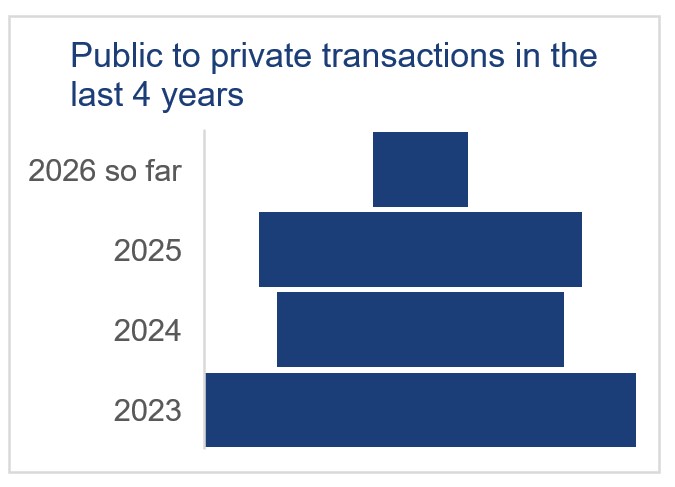

So far in 2026, the level of P2P transactions has been lower than in each of the past four years, possibly reflecting broader market caution and a slowdown in overall deal volumes. The firm offers by private equity firms often talk about the benefit to a company of being taken private. For example, on the offer by EQT Fund Management S.à r.l. for Intertek Group plc, EQT states that the additional flexibility afforded by private ownership would enable Intertek to focus on sustainably improving the long-term value of the business.

Partner, London

Partner, London

Partner, Head of M&A, London

Partner, London

Partner, London

Knowledge Counsel, London

Partner, London

Partner, London

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead