Carbon markets

We examine the evolving landscape of emissions trading systems, as governments and regulators worldwide work to establish effective carbon pricing mechanisms

View more insights

The UK CBAM has been under development since the UK Government announced its intention to introduce a CBAM in December 2023.

In April 2025, the UK Government published draft primary legislation for the UK CBAM (for more detail on this, see our blog post here). This was reviewed in a technical consultation which closed in July 2025, and to which a response was published on 26 November 2025 (the Consultation Response). As part of the Government's 2025 Budget announcement, it confirmed that it will legislate in the Finance Bill 2025-2026 to implement the UK CBAM on 1 January 2027. For more detail on the Budget and its overall impact on infrastructure investment, read our update here.

In this briefing, we summarise the latest updates to the UK CBAM that came out of the Consultation Response.

The Government confirmed that indirect emissions will only start being included in UK CBAM from 2029 at the earliest, in light of concerns around the complexity and administrative challenges associated with reporting on indirect emissions. Indirect emissions include electricity used in producing UK CBAM goods, whether it is generated on-site or off-site. The exclusion of indirect emissions is a different approach to that taken in the EU CBAM, which currently includes indirect emissions for cement and fertilisers.

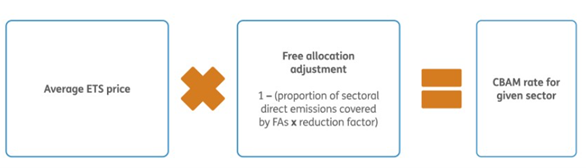

The Government has made some updates to the calculation of the CBAM rate. Previously, the CBAM rate was based on the UK ETS carbon price, which was multiplied by embedded emissions. However, the original calculation contained no adjustments for free allowances. Based on consultation responses, the Government decided to amend this approach and take free allowances into account when calculating the CBAM rate. This "Free Allocation Adjustment" will be on a sectoral basis, according to the free allowances available to each sector each year. This aims to prevent entities from receiving double-protection in respect of carbon leakage, which would weaken the carbon price.

In parallel, the UK ETS Authority has announced the gradual phase out (over a 9-year period) of free allowances for sectors covered by UK CBAM (for more information, read our update here). In light of this, the CBAM rate calculation will also include a sectoral "reduction factor", adjusted annually to reflect the gradual phase out of free allowances.

Source: Factsheet: Carbon Border Adjustment Mechanism

In the 2025 Budget, the UK Government recognised the importance of refineries for the UK's industrial base, as well as for its energy security. Whilst refineries are not currently included in CBAM, the Government has committed to publish a Call for Evidence for the fuel sector in due course.

As part of the consultation response, the following technical changes have also been introduced.

Legislation on UK CBAM was introduced in the Finance Bill 2025-2026 which is currently making its way through parliament, and will apply from April 2026.

HMRC will publish draft secondary legislation, which will be subject to review through further technical consultations in early 2026.

The UK CBAM will come into force from 1 January 2027. Ahead of this date, the UK Government has confirmed its intention to work closely with stakeholders to ensure that guidance is clear and comprehensive before it is published.

We examine the evolving landscape of emissions trading systems, as governments and regulators worldwide work to establish effective carbon pricing mechanisms

Partner, London and Israel Group

UK Head of ESG, London

Senior Associate, London

The articles published on this website, current at the dates of publication set out above, are for reference purposes only. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action.