Stay in the know

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead

Subscribe now

Disputes arising from construction projects are commonly resolved by arbitration. According to HKA's CRUX Insight, principals and contractors claiming against each other for costs and losses associated with damage, defects and delays form a large proportion of the international caseload. However, there is often another avenue for recourse for damage and delays: insurance.

When arbitrating construction claims, a complex interplay often arises between claims between principal and contractor, and claims with insurers. A principal who focuses on one to the exclusion of the other can inadvertently create a gap in recovery, leaving money 'on the table'. Unfortunately, this is a situation that arises all too often, particularly where the respective claims are handled by different teams within their organisation, without coordination.

Developing a holistic recovery strategy, addressing claims against both the contractor and insurers, allows principals to assess the relative strengths and priority of the claims, make informed decisions when conducting both claims, and maximise overall recovery.

This article explores some of the key aspects of the interplay and the tensions that arise when a principal has both an insurance claim and a claim under the construction contract. While the principles discussed in this article are those found in common law, there may be similar principles in contracts subject to other systems of law.

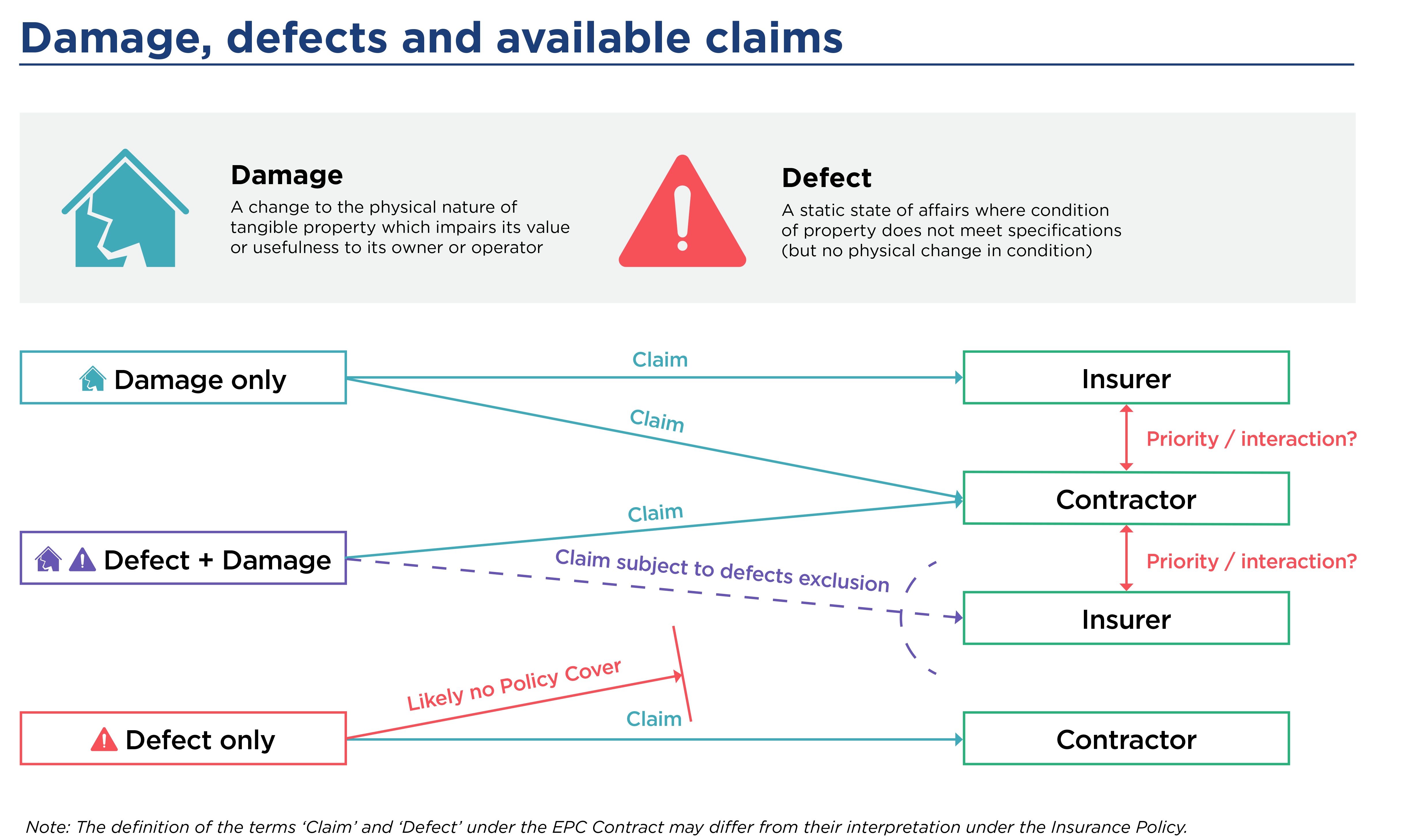

In relation to claims against a contractor, most construction contracts incorporate various mechanisms that allow the principal to require the contractor to rectify quality or performance issues or pay for the rectification of the identified issue. For example, construction contracts often contain express defects liability periods within which a contractor is required to rectify defects, as well as express indemnities for the costs of repairing physical damage to the project. A principal may also be able to claim general damages for breach of contract, where such claims are not excluded by a 'sole remedy' regime. For delay-related losses, construction contracts often provide a right to liquidated damages, being a specific (daily) amount to be paid by the contractor to the principal for delays to project completion.

Insurance cover for damage and delay will typically be addressed by a 'Construction All Risks' (CAR) policy. A CAR policy provides cover for repairing damage to the project under construction. The policy may also include delay in start-up (DSU) cover for loss of revenue due to delays to project completion as a result of the insured damage. This policy will typically be taken out by the principal or head contractor but will name as insured others involved in the project such as contractors, subcontractors, suppliers, and financiers. For the purposes of the remaining sections of this article, we assume a scenario in which the policy is taken out by the principal.

Although construction contracts and insurance provide separate avenues for recovery, neither should be considered in isolation of the other.

Managing these interplays to maximise recoveries is therefore critical. Importantly, principals need to progress claims – whether under the construction contract or insurance – based on a holistic strategy incorporating both:

Each claim can then proceed in parallel and in a way which avoids needlessly prejudicing the other. Ideally, the principal can leverage the contractor's interest in arguing against there being defects to reinforce the principal's position in the insurance claim (and do the same in reverse). This can often lead to an overall settlement with all parties.

Absent any agreement, proceedings against the contractor and the insurer may be necessary. In practice, many developed international arbitration rules are well-equipped to manage this situation and the related interplays. For example, through a case management stay of one set of proceedings over another, or through coordinated proceedings where a common tribunal can determine both proceedings. However, a principal may ultimately need to prioritise one avenue of recourse over another. This decision will normally be based on an assessment of the strength of evidence, the likelihood of financial recovery and other commercial factors.

Another key practical takeaway is that when a construction dispute involving some form of physical damage arises, it is important for both principals and contractors to seek the expertise not only of their legal teams in managing arbitrations, but also of their insurance team in managing insurance claims. This approach ensures that a fully integrated recovery strategy is formulated that effectively harnesses the relevant internal experience and expertise.

.2025-10-15-11-46-16.png)

Partner, Singapore

Partner, London

Partner, Head of Disputes, Middle East, Dubai

Senior Associate, Sydney

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead