Transactions

The value of everything

View our insights

Despite early optimism that M&A would rebound at the start of the year – our UK report this time last year was titled "At a turning point?" – the activity we hoped for did not materialise, and the start of 2025 was very quiet, largely due to economic and geopolitical uncertainty. The second half of the year, however, was dramatically different with the summer in London being one of the busiest in memory, with no opportunity for the lull that we are used to. But we did also see a lot of time spent on deals that never got across the finish line.

Despite the busy second half of the year, the number of deals in 2025 was down on 2024 – we saw a drop of 13%, with the biggest falls in domestic M&A. However, larger deals drove activity. On both inbound and outbound M&A, while steady by volume, we saw significantly higher deal values than in 2024. Most notable were US buyers, who were involved in deals with an aggregate value higher than that for all domestic UK M&A. The number of mega deals (over £1 billion) continues to rise, with 20 in 2023, 31 in 2024 and 34 in 2025.

In terms of sectors, financial services accounted for 30% of deal value, with some significant deals in the insurance sector in particular, including Athora’s acquisition of Pension Insurance Corporation announced in July with a deal value of approximately £5.7 billion. This was followed by real estate, with deals including Unite Group’s £625.7 million acquisition of student accommodation provider Empiric Student Property announced in June.

Consumer was the most active by volume, due largely to professional services deals (including for example Dawsongroup being bought by KKR), followed by tech.

_Regional%20Stats_Update16.jpg)

On public M&A, we saw PE bidders return, on 44% of deals in 2025 compared to 31% in 2024, while strategics remained active too. As with 2024, we again saw plenty of competitive situations, including a PE bidder (KKR) – with a cash offer – and a strategic bidder (Primary Health Properties) – with a cash and share offer – both bidding for Assura, and, somewhat unusually, the strategic winning out over the PE firm.

Shareholder activists and active shareholders continue to influence M&A, with two bids being blocked by shareholders in late 2025. And even as the number of public campaigns continues to rise, so too do the private campaigns that the market doesn’t get to hear about.

We have now had over a year of adapting to the new UK Listing Rules (UKLRs) which were introduced in July 2024 to facilitate London-listed companies doing M&A without the need for shareholder approval. The changes seem to have been accepted by the market as a whole, and companies are now able to move more nimbly, on auctions in particular, as they can execute transactions that were previously challenging because of the need for shareholder approvals that listed companies in other markets were not burdened by. We have also seen more smaller significant transactions under the UKLRs than previously, suggesting companies are now willing to undertake deals that they might otherwise have avoided because they would have required shareholder approval (with the associated additional cost, time and uncertainty) under the old rules.

On merger control, 2025 saw a new chair of the Competition and Markets Authority (CMA) and shortly afterwards a new “4P” approach announced – pace, predictability, proportionality, and process – aimed at boosting growth, investment, and business confidence. This led to a wave of revisions to the CMA's guidance to introduce more business-friendly processes, with more expected in 2026. The government is also consulting on legislative changes to build on the CMA’s ‘4Ps’ initiative. However, merging parties should not interpret these trends as a complete relaxation of scrutiny.

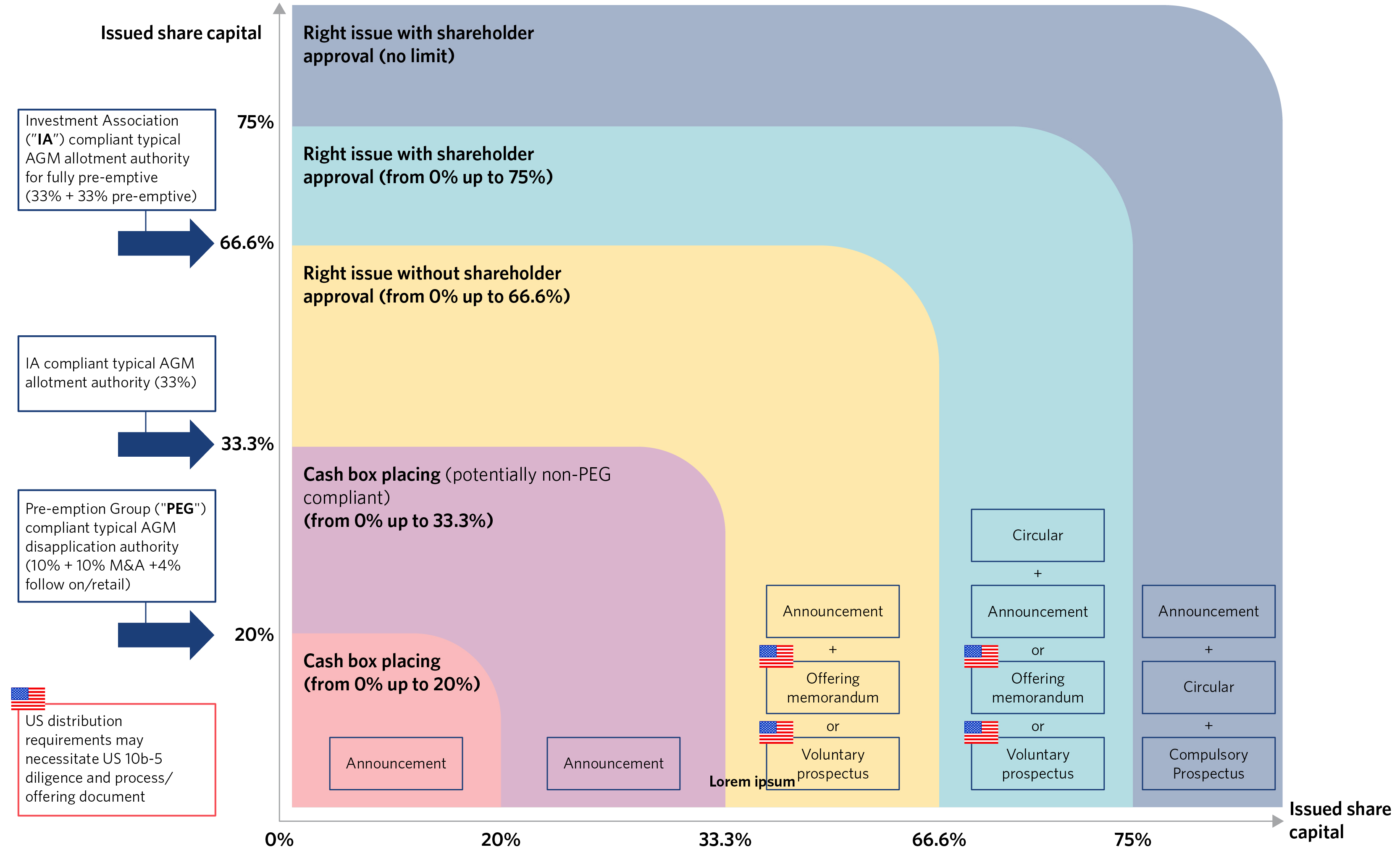

As we move into 2026, we have a new regime for public offers of securities and prospectuses. Listed companies can now issue shares representing up to 75% of their existing listed share capital without having to publish a prospectus. This means that companies will be able to use their shares as consideration much more easily on M&A – potentially up to 66% of their share capital (being the maximum authority to allot shares the Investment Association allows companies to take at their AGMs annually) without having to produce a circular. It will be interesting to see how that plays out in practice and in particular how the market responds to it and what practice develops in relation to disclosure on these deals.

We are optimistic the more business-friendly regulatory environment will give parties greater confidence to do M&A – whether its purpose is to drive transformation, refocus priorities or scale up.

The M&A market was disrupted last year as tariffs and geopolitical issues were digested, and PE sponsors were quiet, but strategic imperatives are asserting themselves with larger cap transactions hopefully fuelling confidence (although we have been here before…).

Deals will undoubtedly continue to take time, and skill, to get over the line but, as we have seen in recent years, the M&A market is used to having to be resilient and adapt to an ever-changing environment.

Partner, Head of Equity Capital Markets, London

Knowledge Counsel, London

Partner, London

Partner, London

The value of everything

The contents of this publication are for reference purposes only and may not be current as at the date of accessing this publication. They do not constitute legal advice and should not be relied upon as such. Specific legal advice about your specific circumstances should always be sought separately before taking any action based on this publication.

© Herbert Smith Freehills Kramer 2026

Receive timely insights and briefings from HSF Kramer, tailored to keep you informed and ahead